The e-way bill system just got its biggest upgrade since launch. A new portal, mandatory multi-factor authentication, stricter validity rules, and automated enforcement mean that what worked in 2024 may not protect you in 2026.

What Is an E-Way Bill and Why It Still Matters

An e-way bill is a mandatory electronic document under India's GST framework, required for transporting goods valued above ₹50,000 between or within states. It serves as a digital declaration to tax authorities — confirming what is being moved, where it is going, who is transporting it, and what the goods are worth.

Since its nationwide rollout in 2018, the e-way bill rules India framework has progressively tightened. In 2025 and 2026, that tightening has accelerated significantly. Enforcement is now more automated, the portal infrastructure has been upgraded, and the compliance margin for errors has narrowed considerably.

For transporters operating across India — whether moving raw materials, FMCG goods, industrial cargo, or consumer deliveries — understanding the current state of e-way bill 2026 rules is not optional. Non-compliance carries financial penalties, vehicle detention, and in serious cases, goods seizure.

What Changed: The Key E-Way Bill 2026 Updates

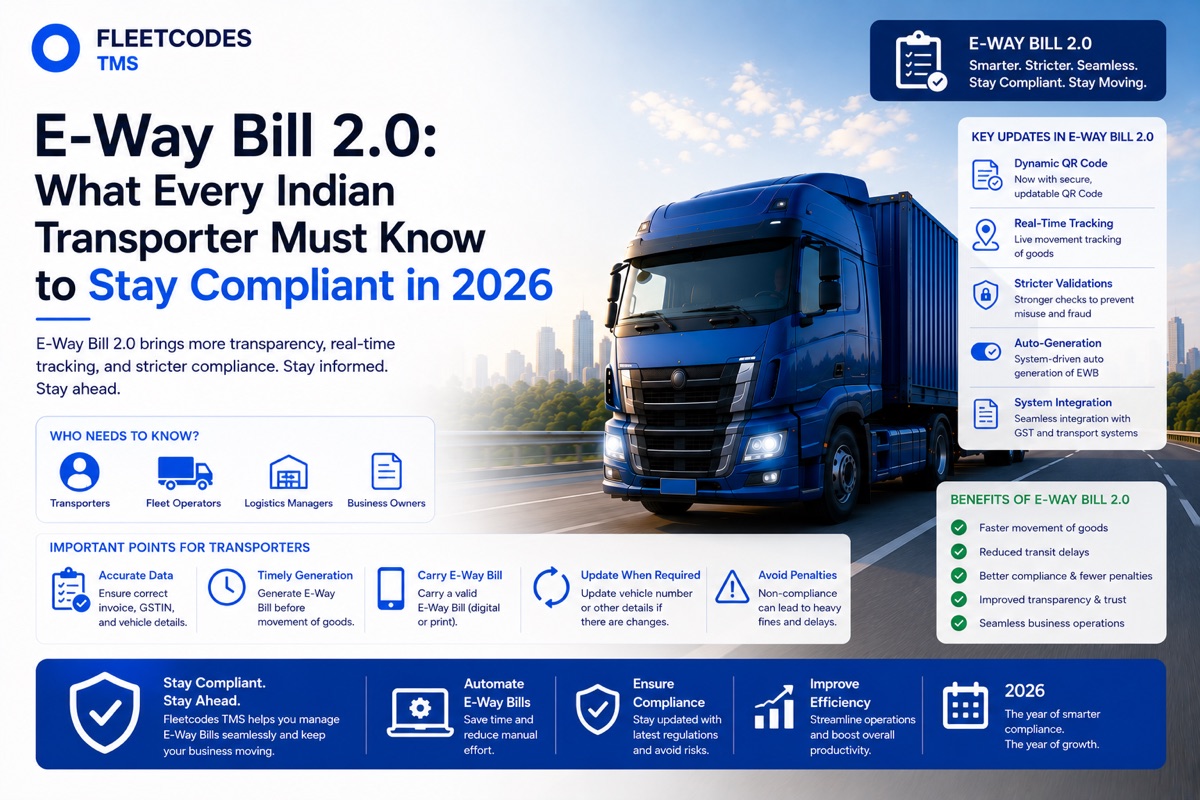

E-Way Bill 2.0 Portal — The New Infrastructure

The most significant infrastructure change is the launch of the E-Way Bill 2.0 portal at ewaybill2.gst.gov.in in July 2025. This new portal runs in parallel with the original at ewaybillgst.gov.in. Both are real-time synchronised — e-way bills can be generated, updated, extended, or cancelled on either platform.

The practical benefit is reliability. The original portal experienced periodic downtime during high-volume periods — particularly at month-end — which caused genuine operational disruption for transporters generating bulk e-way bills. The 2.0 portal was specifically designed to distribute system load and improve uptime.

What you need to do: Ensure your team is registered and can access both portals. If you rely on a single portal and it experiences an outage during a critical dispatch window, the backup portal is your operational safety net.

Mandatory Multi-Factor Authentication

MFA login is now mandatory for all e-way bill portal users. Logging in requires a username, password, and an OTP sent to the registered mobile number. Single-factor login is no longer accepted.

This creates operational friction in two common scenarios:

Scenario 1: A staff member handling e-way bill generation leaves the business. If their mobile number was the registered contact on the account, the business loses portal access until updated — causing delays at dispatch.

Scenario 2: A transport office in a location with intermittent mobile signal. If OTP delivery is unreliable, so is e-way bill generation.

What you need to do: Audit all portal user accounts. Ensure registered mobile numbers are current. Set up at least two authorised users per GST registration so access is never dependent on one person.

The 180-Day Invoice Rule

E-way bills can no longer be generated against invoices that are more than 180 days old. The system enforces this automatically — the portal will reject the generation attempt entirely.

This affects businesses with outstanding or delayed invoices going back several months. Any consignment needing to move under an old invoice will require a fresh invoice before the e-way bill can be generated.

What you need to do: Audit any pending consignments against old billing records. If you have freight moving under historical invoicing arrangements, ensure invoices are current before dispatching.

Automated Portal Validations

In 2026, the portal enforces several automatic checks before allowing e-way bill generation:

- GSTIN status validation — if the supplier's or recipient's GSTIN is cancelled or suspended, the portal rejects the bill

- Invoice date check — the 180-day rule is enforced automatically

- Distance and validity auto-calculation — validity period is calculated from the distance entered (1 day per 200 km for standard cargo; 1 day per 20 km for over-dimensional cargo)

- HSN code validation — incorrect or outdated HSN codes trigger automatic rejection

These checks mean that errors which previously went undetected until a checkpoint inspection are now caught at generation — better for compliance, but only if your underlying data is accurate.

The 360-Day Extension Cap

E-way bill validity can be extended when a consignment is delayed. However, a 360-day cap on cumulative extensions per e-way bill was introduced in 2025. For most standard consignments this is academic — but for project cargo, out-of-gauge equipment, or complex multi-modal movements, it is worth understanding.

E-Way Bill Validity Rules: Quick Reference

Understanding how long your e-way bill is valid is operationally critical. An expired bill at a checkpoint is one of the most common and most avoidable compliance failures.

| Cargo Type | Validity Per Distance | |---|---| | Standard goods (road) | 1 day per 200 km (minimum 1 day) | | Over-dimensional cargo | 1 day per 20 km | | Non-motorised transport | 1 day per 20 km | | Multi-modal transhipment | Additional 1 day per transhipment point |

Validity starts from the time of generation and expires at midnight on the last valid day. If a consignment is delayed and will not reach its destination in time, the extension must be applied before expiry — not after.

Extending a bill: Extensions can be initiated within 8 hours before expiry and up to 8 hours after expiry. Beyond this window, the bill cannot be extended and a new one must be generated — which creates serious documentation problems for in-transit goods.

E-Way Bill Penalty India: What Non-Compliance Actually Costs

| Violation | Penalty | |---|---| | Moving goods without e-way bill | ₹10,000 or tax evaded — whichever is higher | | Incorrect details on e-way bill | ₹10,000 | | Expired e-way bill during transit | ₹10,000 | | Tax evasion confirmed at inspection | 200% of tax evaded | | Vehicle detained at checkpoint | Held until penalty paid and compliance restored |

For high-value consignments, the 200% tax evasion penalty is the most serious risk. A ₹10 lakh consignment with 12% GST carries a tax liability of ₹1.2 lakhs — and a 200% penalty of ₹2.4 lakhs if intercepted without a valid bill. Beyond the fine, vehicle detention during peak logistics periods cascades into customer delivery failures that damage commercial relationships far beyond any monetary penalty.

Transporter-Specific Responsibilities Under E-Way Bill Rules

Transporters have distinct obligations that differ from shippers and recipients:

Part B completion is your responsibility. When a supplier generates Part A of the e-way bill, the transporter must complete Part B — entering the vehicle number before goods depart. If the supplier has not generated Part A, the transporter is responsible for generating the complete bill.

Consolidated e-way bills for multi-consignment vehicles. When a single vehicle carries multiple consignments on the same journey, a consolidated e-way bill covers all of them. This is especially relevant for part-load operators and LCL movements.

Updating vehicle number mid-journey. If goods are transhipped to a different vehicle due to breakdown or operational reasons, the vehicle number on the e-way bill must be updated before the goods continue moving. Failure to update is treated as missing documentation.

Verification before departure. Transporters are expected to verify that the e-way bill details match the physical goods, vehicle, and consignment documents. Discrepancies discovered at checkpoints are the transporter's problem — regardless of where the error originated.

Intra-State E-Way Bill: State-Wise Threshold Summary

While the inter-state threshold is a uniform ₹50,000 across India, intra-state thresholds vary by state:

| State Category | Intra-State Threshold | |---|---| | Standard states (most) | ₹50,000 | | Maharashtra, Tamil Nadu (selected goods) | ₹1,00,000 | | Delhi, Gujarat (selected categories) | ₹1,00,000 | | Some NE states | Exempt or higher threshold |

Transporters operating across multiple states must know the specific intra-state rules for each state they serve. Applying the inter-state standard everywhere is a common compliance gap for multi-state operators.

Pre-Dispatch Compliance Checklist

Before every dispatch, verify:

- E-way bill has been generated and Part B is complete with the correct vehicle number

- E-way bill validity covers the expected journey duration (factor in route-typical delays)

- GSTIN of supplier and recipient are active

- Invoice date is within 180 days

- HSN code matches the goods being transported

- Driver has the e-way bill number — print or digital — and can produce it at checkpoints

- For multi-stop movements: separate e-way bills or consolidated e-way bill as appropriate

- For long routes: expiry alert set in case extension is needed en route

The Case for Automated E-Way Bill Management

For operations running dozens or hundreds of trips per day, manual e-way bill generation is both a compliance risk and an operational bottleneck. Every manual data entry is a potential error — a wrong GSTIN, an outdated HSN code, an invoice that slips past the 180-day threshold.

Automated e-way bill generation, integrated directly into your dispatch workflow, eliminates the most common error sources:

- Consignment details flow from the booking record to the e-way bill portal — no re-entry

- GSTIN validation happens at booking, before dispatch day pressure

- Validity tracking with automatic expiry alerts protects in-transit compliance

- Extension reminders can be triggered based on GPS-tracked trip progress

This kind of transport compliance GST India automation was once the domain of large enterprise TMS platforms. In 2026, cloud-based tools bring it within reach for fleets of any size. The investment is invariably smaller than the cost of a single serious compliance failure — and dramatically smaller than the cumulative cost of the dozens of smaller violations that manual operations absorb silently every month.

FAQs

What is the e-way bill limit in 2026? The core threshold remains ₹50,000 for inter-state movements. For intra-state movements, thresholds vary by state — typically ₹50,000 to ₹1,00,000 depending on the state and goods category.

What is E-Way Bill 2.0 and how is it different? E-Way Bill 2.0 is the new portal at ewaybill2.gst.gov.in, launched July 2025. It runs in parallel with the original portal, with real-time synchronisation, offering better uptime and reliability for high-volume users.

What is the penalty for moving goods without an e-way bill in India? ₹10,000 or the amount of tax evaded, whichever is higher. Where tax evasion is established, the penalty rises to 200% of the tax evaded. Vehicles can be detained until the penalty is paid.

Can e-way bills be generated on a mobile phone? Yes. The GST portal has a mobile-accessible interface. API-based integrations also allow generation from within transport management software. The registered mobile number must be available for MFA regardless of device.

What should a transporter do if the e-way bill expires mid-journey? Extension can be applied within 8 hours before and up to 8 hours after expiry. If the window is missed, contact the nearest GST office and regularise documentation as quickly as possible to avoid detention.

How does the 180-day invoice rule affect day-to-day transport operations? Transporters should confirm that any consignment they carry is backed by a valid, current invoice before departing. An invoice older than 180 days will cause e-way bill generation to fail at the portal — holding up the entire consignment.

This guide covers the key e-way bill changes every Indian transporter needs to act on in 2026. For operational questions specific to your fleet or routes, consult your GST practitioner for guidance on your specific compliance situation.